The State of the Startup and Venture Ecosystem in Colorado 2020

Calling the Colorado startup ecosystem our home turf, we on the Access Ventures team often get asked by out-of-towners, “how is the venture scene in Colorado?” or hear comments like “it seems like there is a lot of activity out there.” Fortunately, a lot has been going on but unfortunately, I’ve never really had a strong, factual response in these situations. This post seeks to paint what I hope to be a fairly thorough picture of the current state of the Colorado startup and venture community heading into 2020… if for no other reason than to self-servingly help me better engage in such a conversation!

A rapidly growing ecosystem

Significant lift in venture dollars

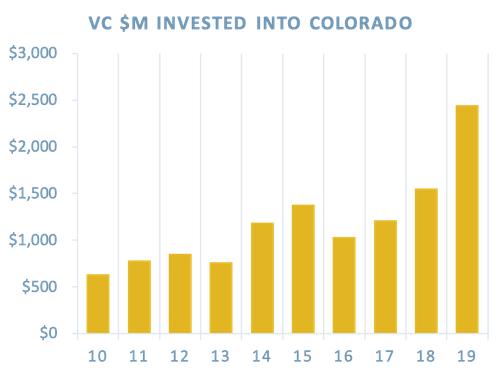

2019 was a big year for Colorado startups. In total, $2.5B of venture dollars was invested into the centennial state, a big 1.5x lift on 2018 ($1.6B) and a 2.3x bump on 2016 ($1B).

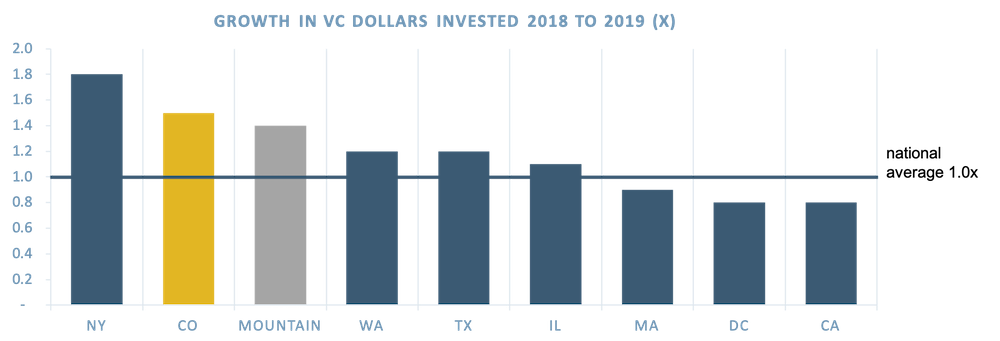

This growth in capital invested surpassed most other major investment states and far exceeded the national baseline, which saw a slight overall decline in total VC dollars on 2018 and a lower 1.8x rise on 2016.

Huge growth in deal volume

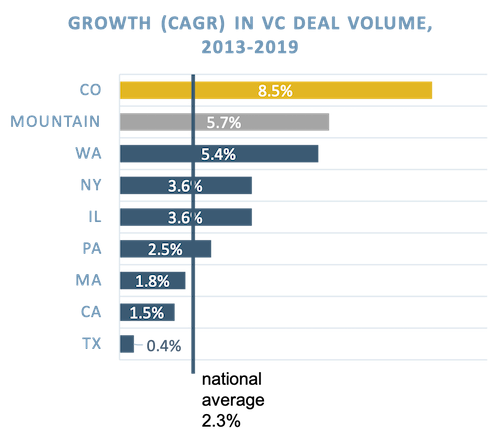

Perhaps more impressive than the increase in investment dollars is the rise in actual deal volume. Since 2013, Colorado has seen an 8.5% average annual increase (CAGR) in the number of companies getting funded per annum. This is in fact, by a significant margin, the fastest growth of any major venture state in the country (states with 100+ annual deals — 23 in total), and almost 4x the national growth rate in deals over the same time period.

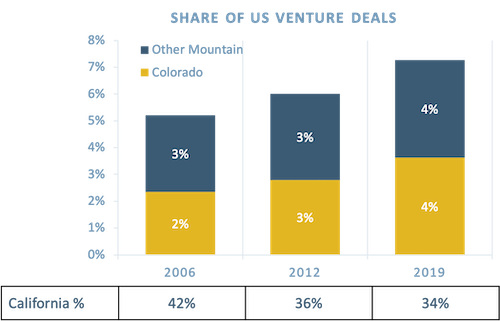

With this rapid growth in activity, Colorado now accounts for over 4% of national venture deals, up from 2% in 2006. The mountain region now accounts for over 8% of nationwide investments, whilst California has declined from accounting for 42% to 34% of deals during the same time period.

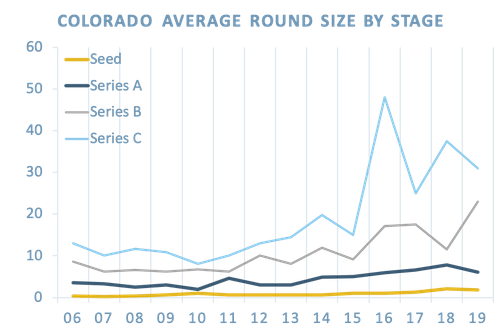

Increasing deal sizes

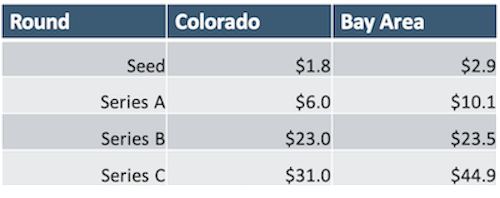

Increased deal sizes are inline with national themes, there has also been a shift in the size and profile of deals happening in Colorado over this time. The average seed deal in Colorado was $1.8M in 2019 versus $400K in 2006. Series A, B, and C deals averaged $6M, $23M, and $31M retrospectively, all effectively doubling in size since 2006 as well.

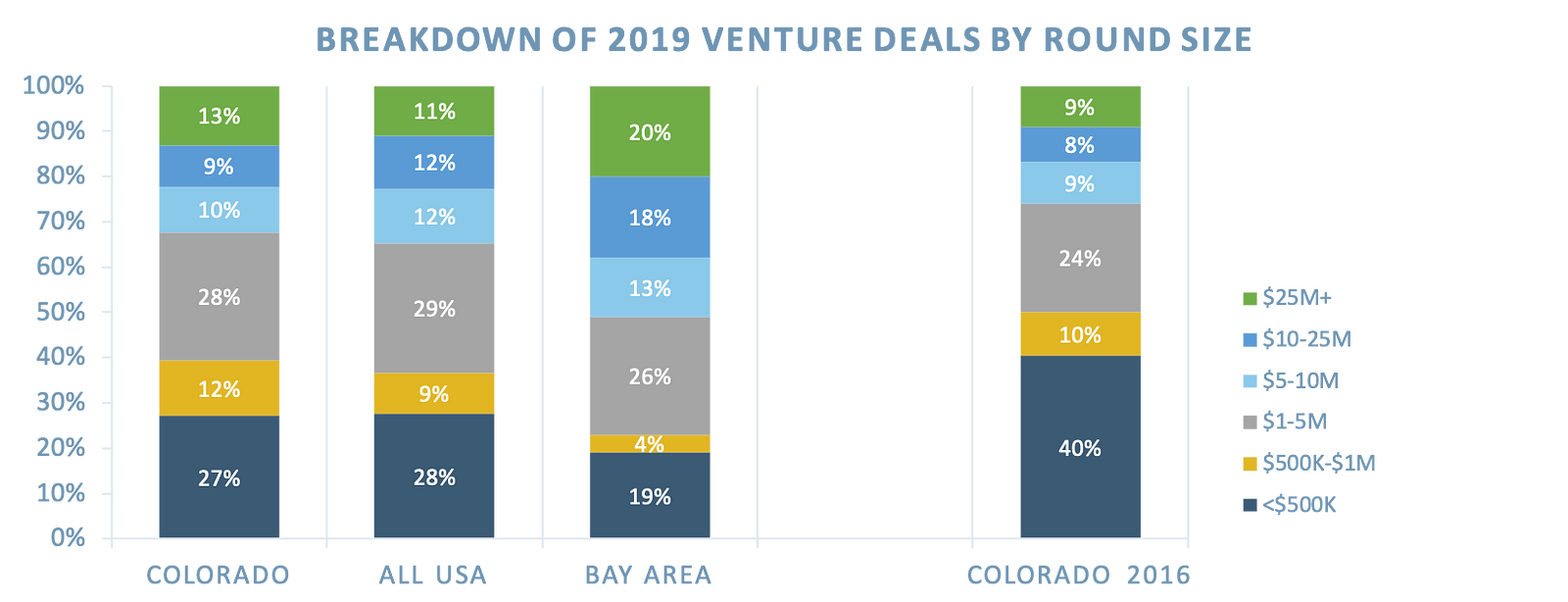

In 2016, 40% of investment rounds were <$500K; that number was down to 27% by 2019, reflecting a maturing market with bigger and later-stage deals taking place in the State.

On average, Bay Area companies tend to raise more money at each stage of the fundraising evolution — seed, Series A, etc.

However, the size of the rounds is largely meaningless — bigger rounds don’t signify or correlate strongly to companies with greater promise or bigger exits. In fact, a primary driver of larger early-stage rounds in the Bay Area is actually quite simply the higher cost base there. $1M raised by a Bay Area company is worth $1.31M to a Denver company in terms of purchasing power parity (the lower cost to achieve the same business investments in staff, office space, etc), meaning companies in Colorado can (and should) be raising less to achieve the same outcomes for investment through pure capital efficiency.

What is obviously more important than the size of rounds is the outcomes achieved for the stakeholders involved. And the reality here is that 1) big exits are capable of, and actually are, taking place in the mountain region and 2) those exits are in general occurring more efficiently — on average, the data suggests that by the time founders have hit their Series C, they have suffered ~4.2% extra in dilution in the Bay Area versus Colorado (i.e. the larger round sizes, even despite the larger on average first stage pre-money valuations, means they have suffered more equity dilution by this point).

Bigger exits are taking place

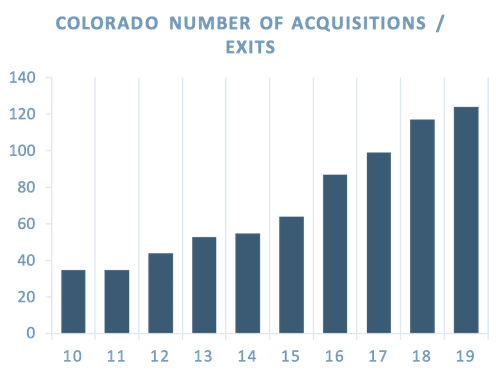

Over recent years, Colorado and the mountain region more broadly has also been seeing solid growth in exits — both by number and size. In fact, in 2019, companies in the mountain region exited for an average of $429M (n=38 known exit values) versus $235M (n=183) in the Bay Area. A statistic like this is a little misleading and can be very skewed by a few large or small outlying outcomes, and I hesitate in sharing it. To be clear, the only takeaway here should be that big exits are capable of happening in places like Colorado outside the Bay Area; definitely not to suggest that bigger exits happen on average in Colorado.

The region has also seen a steady rise in the number of exits over the years.

10 years ago, it would have been difficult to point toward many major tech exits in the State, let alone unicorns. Yet, if my numbers are correct, 4 new Colorado companies joined the unicorn league tables in 2019 alone — Guild, Ibotta, Evercommerce, and Ping Identity.

The key drivers of growth

A couple of factors are at play in fueling this impressive growth in the centennial state startup ecosystem:

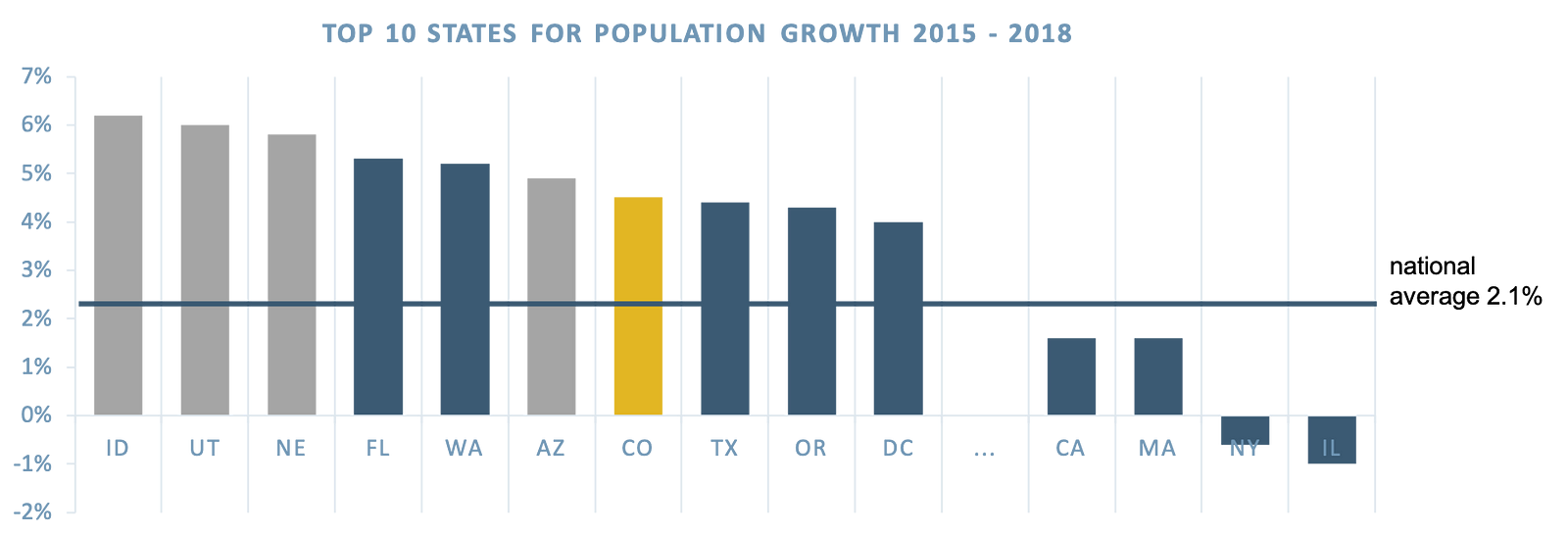

First —no doubt a big driver of growth has been underlying population growth. From 2015–2018, the population of Colorado grew over 5%, making it the 7th fastest-growing state in the country with more than double the national growth rate. Colorado has effectively been seeing over 250,000 people move into the state each year, driving average net migration of well over 100,000 people per annum. The mountain region, in general, has been the fastest region of growth in the country with 5 of the top 10 states.

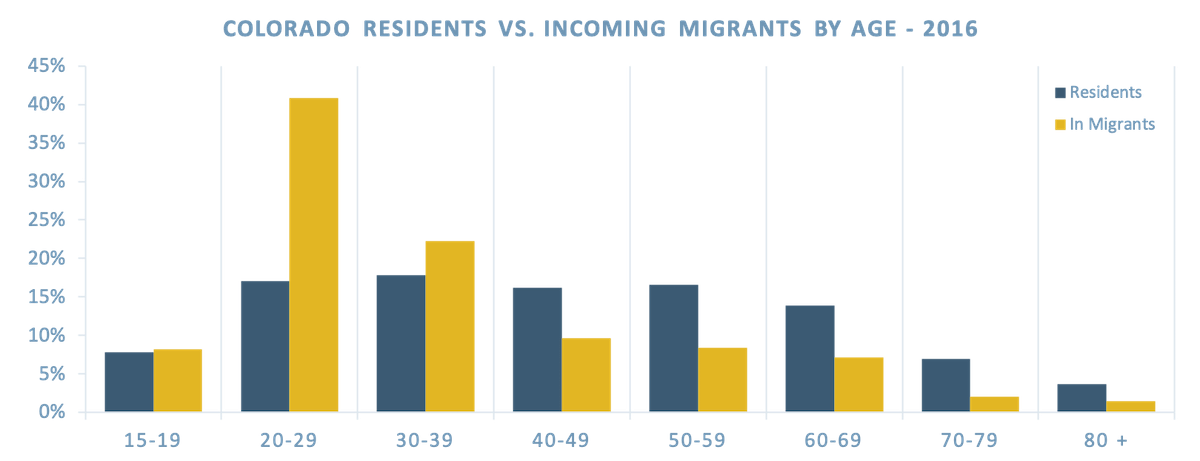

Equally important is the profile of this population growth, which has been largely younger, educated, and skilled labor. 71% of over 15-year-old migrants to Colorado are aged between 15 and 39 when that age segment only accounts for 43% of the existing base of residents.

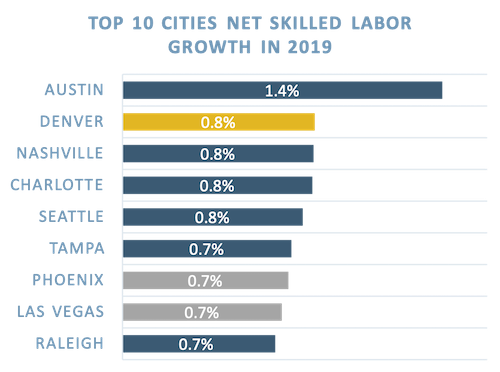

In addition — 79% of these migrants who are over 25 have some form of college education. According to a Linkedin report for 2019, Denver was the second city in the country for “net labor migration” (calculated as (1) # of members that moved to Denver minus (2) # of members that left, divided by (3) starting base of members).

In sum — the people coming in are young, educated, and on Linkedin.

Second — perhaps in part attracted by this dynamic and in part causing it, serious coastal tech companies have either moved, set up or growth operations in Colorado in recent years. Slack, Facebook, Salesforce, and others have opened Denver tech hubs.

According to a report from Cushman & Wakefield covering the 89 largest tech companies in the Bay Area (that have 100,000+ SF), 58 have opened an office in the Denver region in recent years and taken up 1M square footage of office space. Today, approximately 7.4% of all employment in the city is in tech (the US average is 4.9%), which is an almost 1% lift on 2018.

For an exploration on why these companies are looking at Colorado for primary or secondary offices, read another piece I wrote on the topic here.

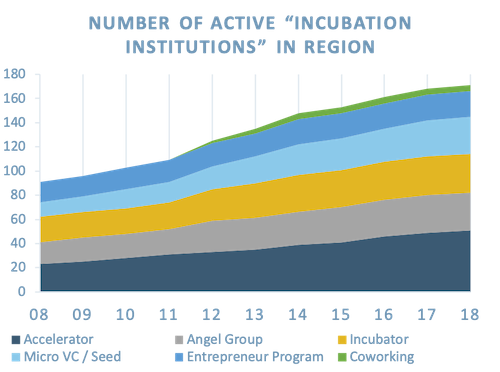

Third — the last decade has also seen the development of fairly robust early-stage support infrastructure for Colorado startups. “Incubation institutions” in the state — including accelerators, angel groups, incubators, etc — have doubled in number in the last 10 years, and the State being home to the likes of institutions such as Techstars no doubt helps.

Areas for Future Development

Despite the above, there is certainly room for improvement in the Colorado ecosystem:

Growth in funding – For one, local funding has not kept up with the pace of growth in fundable startups. This is feedback you will receive from many founders you speak to here, and is certainly played out in the data too. For example:

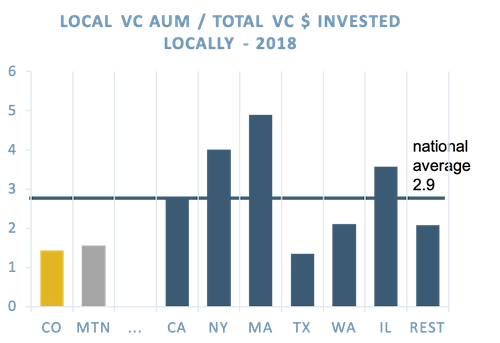

Local venture assets under management compared to venture dollars invested is the lowest of any state in the country.

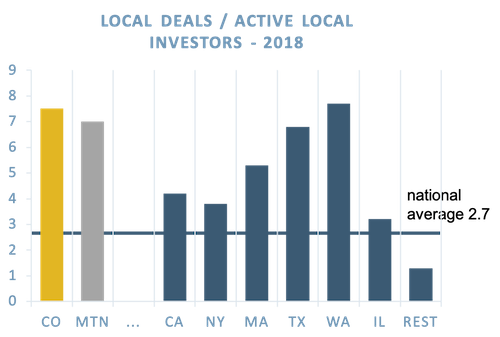

The state also has the highest invested deal volume per local investor of any state in the country too.

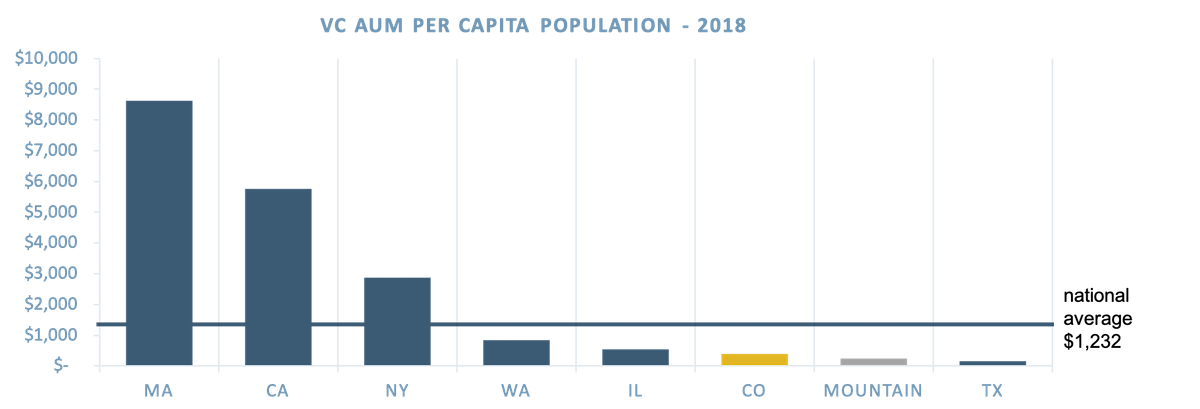

Finally, the state also has one of the lowest local venture communities per capita in the country.

In sum — whilst Colorado has seen significant development in the tech and startup community, it has seen less development on the investment side of the equation. The importance of investor proximity and localization increases the earlier companies are in their lifecycle, and the continued development of the investment community will be important for the continued growth of the startup ecosystem.

Other areas of improvement — there are certainly other areas of improvement of the ecosystem. Looking at the lessons of other thriving ecosystems, some things that will be important for Colorado’s continued growth will be:

- Expanding the talent funnel — Colorado will need to continue to attract young, educated talent from outside the State to migrate in to supplement its talent flow from the local educational system. Don’t get me wrong, the local colleges are fantastic, however Colorado does not have the same breadth and volume of colleges and student flow as say a Boston or Chicago has. Fortunately, the attractiveness of Colorado has meant that to date, it has been able to seduce that talent in. Hopefully, the local colleges will keep extending themselves in key areas of high skills demand such as computer science, robotics, engineering, data science, etc.

- Building stable tech stalwarts — Seattle’s tech ecosystem has been largely built on the shoulders of Microsoft and Amazon. Those companies both attract talent to the city as well as provide the perfect training ground for future founders and operators. Colorado has started to see some of its own promising titans of tech emerge as well as the growth of large secondary offices for the Silicon Valley majors, but this trend will need to continue.

- Growing diversity — finally, the diversity of the community will also be important to the continued growth of the ecosystem. It is well-documented that a significant share of America’s innovation has been driven by immigrants and people of all backgrounds. Reimagining the future requires being openminded and exposed to difference.

For those of you who made it this far, congrats and thanks for reading. Overall, 2019 has been an awesome year. These are some exciting times for the startup ecosystem of Colorado and I, for one, am pumped for what’s to come in 2020! Feel free to reach out with any questions or to discuss.